📉 May CPI Falls 0.3%

💼 Unemployment Holds at 2.9%

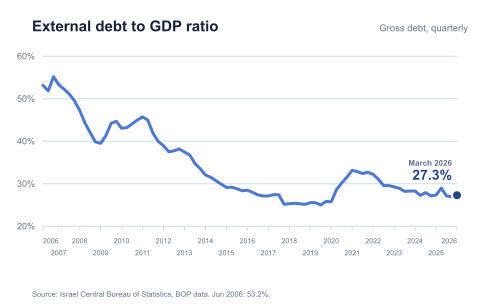

🌐 External Debt Keeps decreasing

|

This week’s economic data from Israel presents a picture of stability. The Consumer Price Index (CPI) declined by 0.3% in May, leaving inflation steady at 1.9%. Trend data points to an annualized inflation rate of 1.4% over the February–May 2026 period, while the average inflation forecast among commercial banks and economic consultancies stands at 1.8% for the year ahead. Taken together, these figures reinforce market expectations that a monetary easing cycle may be approaching, with a potential interest rate cut by the Bank of Israel in the near term.

Labor market indicators continue to signal resilience. The unemployment rate edged up slightly from 2.8% to 2.9% in May, remaining at historically low levels and suggesting underlying stability. At the same time, the job vacancy rate increased from 4.1% to 4.2%, reflecting sustained demand for workers and ongoing tightness in the labor market.

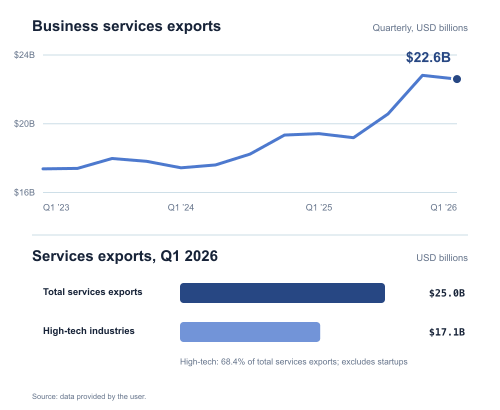

Israel’s Services exports remained a central pillar of Israeli exports, totaling $25 billion and generating a $10 billion surplus in the services account. This surplus reflects Israel’s structural strength as a net exporter of high-value services, providing a stable source of foreign currency inflows that supports exchange rate stability and overall financial resilience. High-tech services exports, excluding startups, reached $17.1 billion in Q1, accounting for 77.3% of total business services exports and highlighting the innovation sector’s dominant role in sustaining this external strength.

Alongside this, capital inflows remain solid. Foreign direct investment accelerated to $14.1 billion in Q1, nearly doubling from $7.6 billion in the previous quarter, while rising valuations of Israeli securities held by foreign investors further contributed to external balances. Israel’s net international liabilities rose modestly by approximately 0.8% in the first quarter, reaching $658 billion, a development that remains well supported by continued inflows and strong export performance.

At the same time, short-term indicators reflect the lingering impact of the war with Iran. The Composite Index of Economic Activity declined by 0.4% in May, influenced in part by weaker retail trade, services, and industrial production during March, which marked the peak of military activity. Additional pressure came from lower imports of consumer goods and reduced indirect tax revenues in May. However, this decline was partially offset by stronger credit card spending, positive financial market performance and an increase in goods exports.

Overall, the combination of a resilient labor market, moderating inflation, and improving financial conditions supports a cautiously optimistic outlook. As the economy transitions out of a period of conflict, these factors are contributing to growing market confidence ahead of the upcoming interest rate decision.

Stay informed and stand with Israel,

Noach Hacker

|

Israel’s CPI fell 0.3% in May, keeping the 12-month inflation at 1.9% - similar to the previus two months. The seasonally adjusted index declined 0.2%. Trend data for February–May placed the annualized inflation rate at 1.4%. Prices decreased in fresh vegetables (4.9%), transportation (2.7%) and furniture (0.4%). Increases were seen in fresh fruit (6.7%), clothing (1.9%), culture & entertainment (1.1%), housing (0.6%).

|

Israel’s services exports reached $25 billion in Q1 2026. Business services accounted for $22.6 billion of that total, driven largely by high-tech industries, which generated $17.1 billion in exports. This performance highlights the continued strength of Israel’s innovation sector.

|

Israel’s gross external debt, measured as liabilities in debt instruments to nonresidents, has been declining in recent years, with the exceptions of COVID-19 and the early months of the Iron Swords war. In Q1 2026, the ratio remained stable, reaching 27.3% of GDP at the end of March. At the same time, Israel maintained a negative net external debt position of approximately $325 billion, meaning the economy holds far more debt assets abroad than it owes to foreign creditors.

|

|

|

|

|

.png)