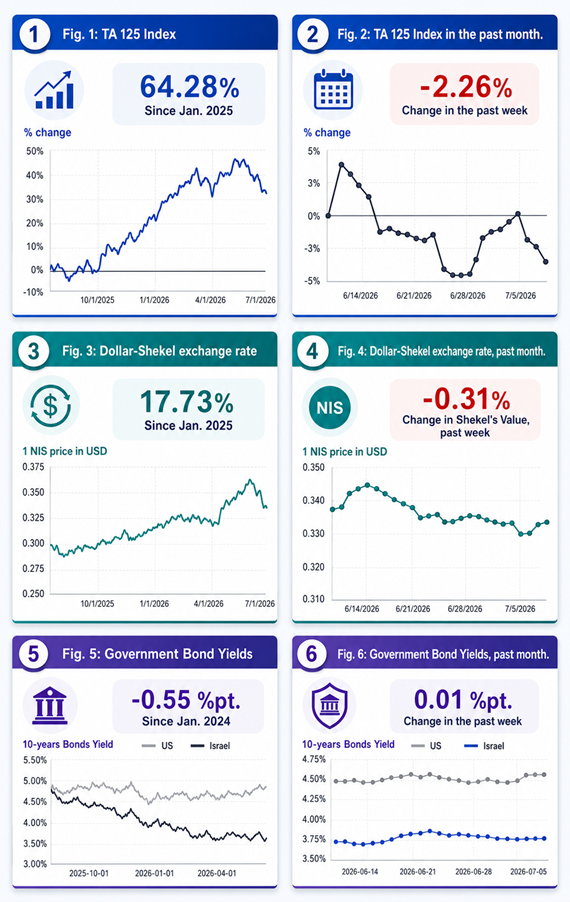

🏦 Bank of Israel cuts rate to 3.5%

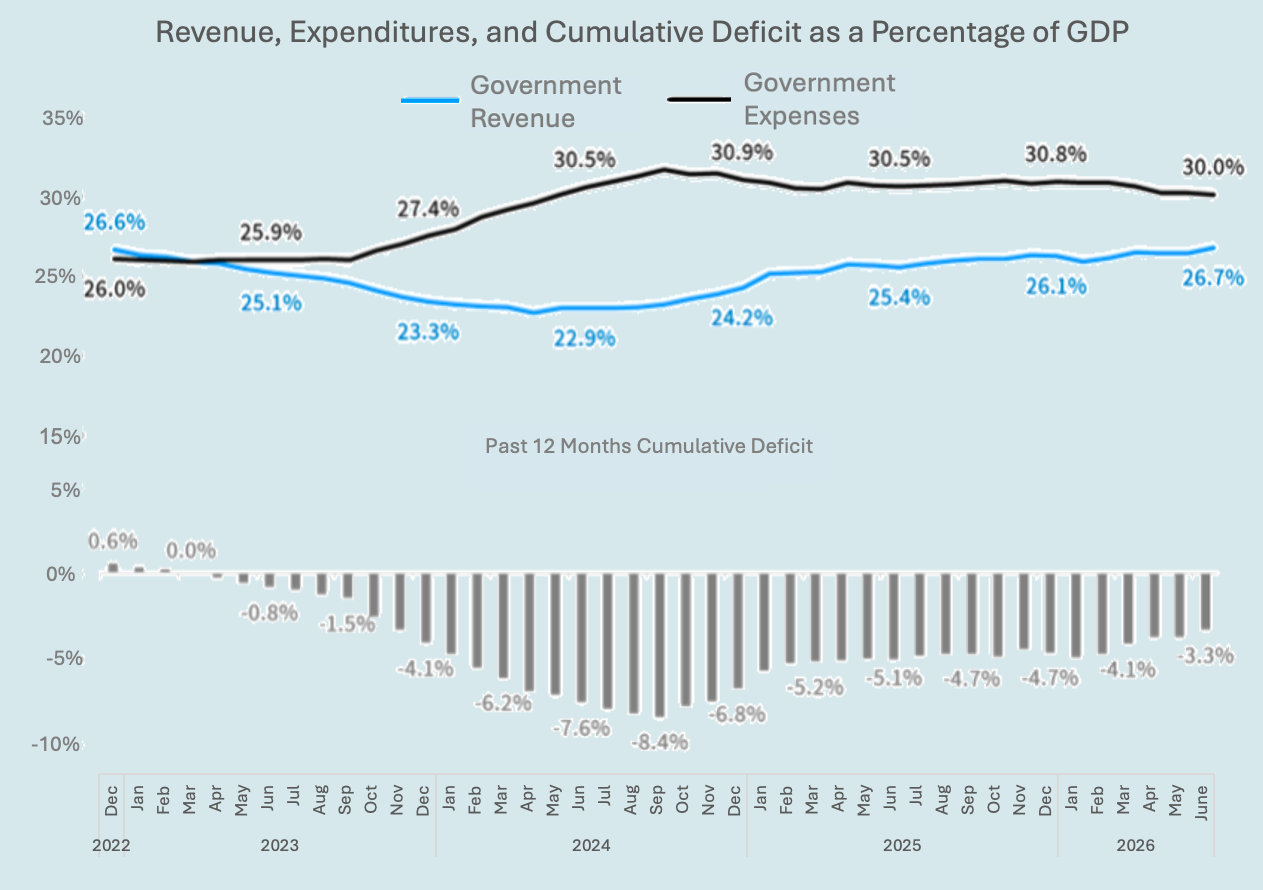

🛡️ 12-month deficit falls to 3.3% of GDP

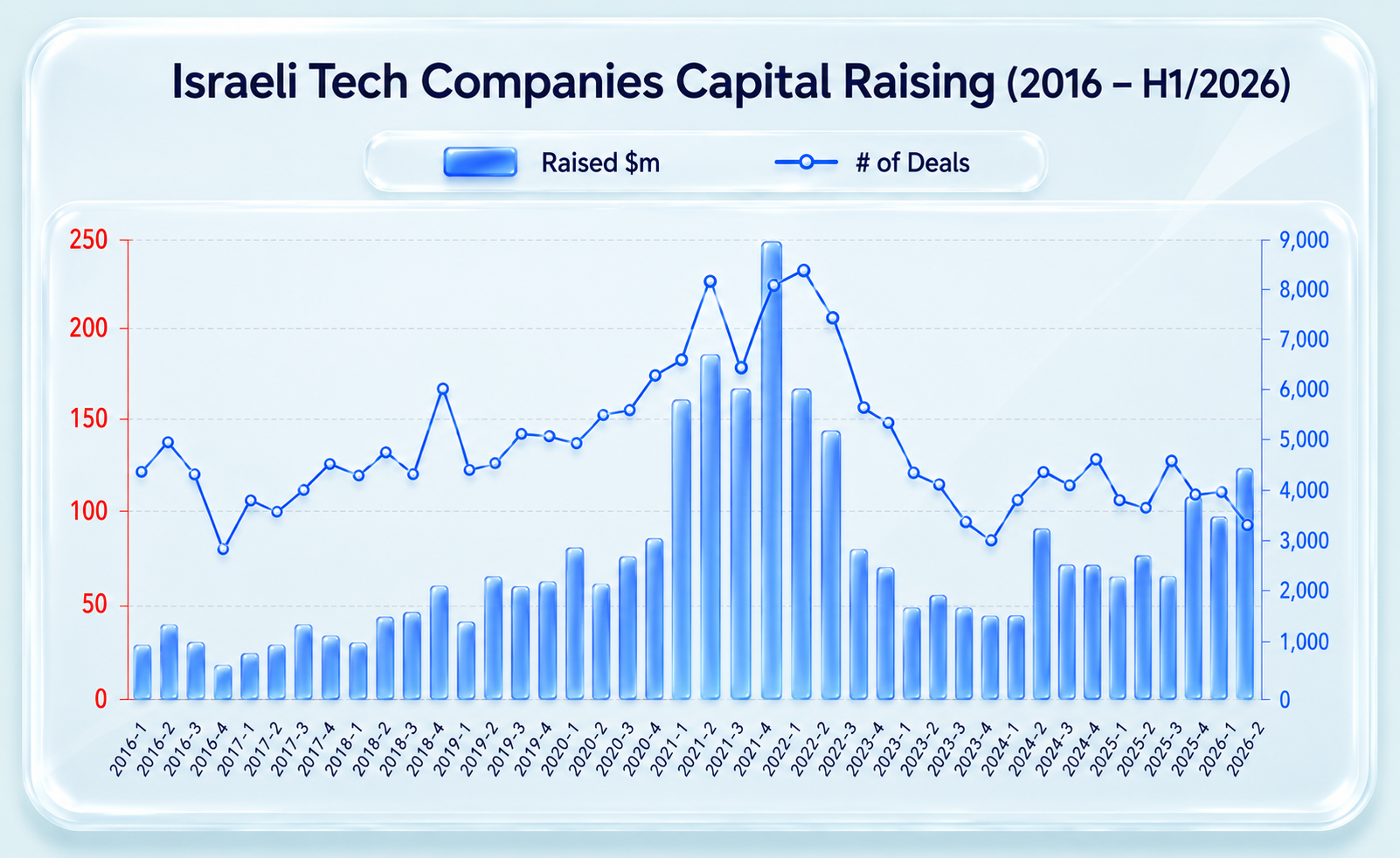

🚀 Q2 tech funding highest since 2022

|

This week, Israel’s economy continues to demonstrate resilience alongside clear signs of expansion across multiple fronts, from macroeconomic policy to high-tech activity and domestic demand.

Budget execution data continues to be positive, pointing to a decline in the annual deficit to 3.3%, driven by higher government revenues and stable expenditure levels.

The government has moved to strengthen key growth engines through a comprehensive program of approximately NIS 1.6 billion, aimed at supporting high-tech, industry, and exporters. The high-tech sector—accounting for 18.3% of GDP and 58% of Israeli exports—has faced headwinds due to the appreciation of the shekel against major trading currencies. In response, the program focuses on improving competitiveness through workforce training, incentives for research and development, and support for the acquisition of advanced equipment, including accelerated depreciation and targeted grants.

Monetary policy has also shifted to support economic activity. The Bank of Israel lowered the interest rate from 3.75% to 3.5%, in a decision based on a favorable inflation environment and confidence in the economic outlook. The Bank’s Research Department now forecasts GDP growth of 4.0% in 2026 and 5.5% in 2027.

In this context, the International Monetary Fund (IMF) also updated its outlook for the Israeli economy. While growth expectations for 2026 were revised downward to 3.5%, from 4.8% in the February forecast following the recent conflict with Iran, the projection still reflects relatively strong growth—above that of most advanced economies and a clear acceleration from 2.9% in 2025. The IMF further expects growth to strengthen to 4.4% in 2027, alongside moderating inflation, which is projected to decline from 3.0% in 2025 to 2.3% in 2026 and 2.1% in 2027.

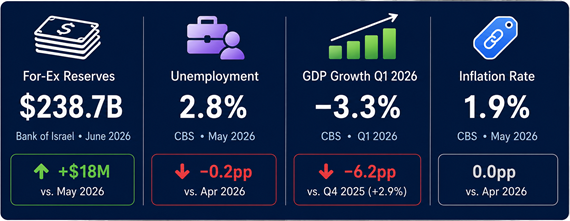

Additional factors supporting the Bank of Israel’s rate decision include low inflation, currently at 1.9%, and expectations of 1.8% inflation in both 2026 and 2027. The labor market remains tight, with wages rising by 6.8% between March and May compared to the same period last year, and the job vacancy rate increasing slightly to 4.2% in May. Public debt is expected to remain below 70% of GDP through the end of the year and stabilize in 2027.

Israel’s foreign exchange reserves continue to provide a strong macroeconomic buffer, rising slightly to $238.7 billion at the end of June—equivalent to 37.2% of GDP. This level reflects a substantial cushion for the economy in the face of external shocks.

Business sentiment surveys indicate improving conditions in June, particularly across construction, retail, and services, while some softness remains in manufacturing and high-tech industries, likely reflecting the impact of the stronger shekel on export-oriented sectors.

Preliminary data from IVC for Q2 2026 highlights renewed momentum in the high-tech sector, with Israeli companies raising over $4 billion—the highest quarterly level since Q3 2022. At the same time, 2025 has already seen a record number of new unicorns, with 16 companies reaching valuations exceeding $1 billion, totaling more than $25 billion in combined value.

Recent indicators further reinforce the positive outlook. Industrial production increased at an annualized rate of 8.4% between February and April, with high-tech manufacturing rising by 16.7% and export revenues surging by 66.4%. Overall business revenues grew at an annualized rate of 2.0%, while high-tech revenues increased by 12.8% and industrial high-tech revenues by 26.9%, pointing to strong external demand and stabilization at elevated levels.

Financial conditions also reflect underlying strength. The public’s financial asset portfolio expanded by NIS 55 billion in Q1, reaching NIS 7.25 trillion, with equity holdings rising by 5.5% and corporate bond holdings by 3.1%.

Finally, private consumption continues to support growth. Credit card purchases increased at an annual real rate of 4.2% between March and May, with spending on goods and services rising by 6.3% and food and beverages by 5.9%, indicating steady demand across key consumption categories.

Taken together, recent data points, for the first time in several weeks, to the economy emerging from the immediate shock of the conflict with Iran and returning to a positive growth trajectory—supported by strong fundamentals, policy support, and continued momentum in its core growth sectors.

Stay informed and stand with Israel,

Noach Hacker

|

The 12-month deficit fell to 3.3% of GDP, while the January-June deficit narrowed to NIS 6.8 billion from NIS 32.4 billion a year earlier. In H1 2026, government revenues rose to 26.7% of GDP from 26.1%, while expenditures eased to 30.1% from 30.5%, helping strengthen the fiscal position.

|

Tech Funding Accelerates in H1

|

Israeli tech companies raised $7.6 billion across 193 rounds in H1 2026, up 52% from H1 2025, according to IVC and LeumiTech’s first H1/2026 Tech Review findings. Q2 alone brought $4.2 billion across 86 rounds, with cyber leading at $2.57 billion and Defense Tech plus Quantum raising $846 million in six months. |

The Bank of Israel now expects GDP to grow 4.0% in 2026 and 5.5% in 2027, lifting its 2026 forecast by 0.2 percentage points from March while leaving 2027 unchanged. The IMF’s July Israel forecast is more conservative at 3.5% for 2026 and 4.4% for 2027, still pointing to a clear pickup from 2.9% growth in 2025.

|

|

|

|

|