🦁 3rd Week of War

💰Record-Breaking Investments

🛡️First Wartime Econ Indicators

|

In the third week of Operation “Roaring Lion” / "Epic Fury" Israel’s economy continues to demonstrate stability in the face of the wartime challenge.

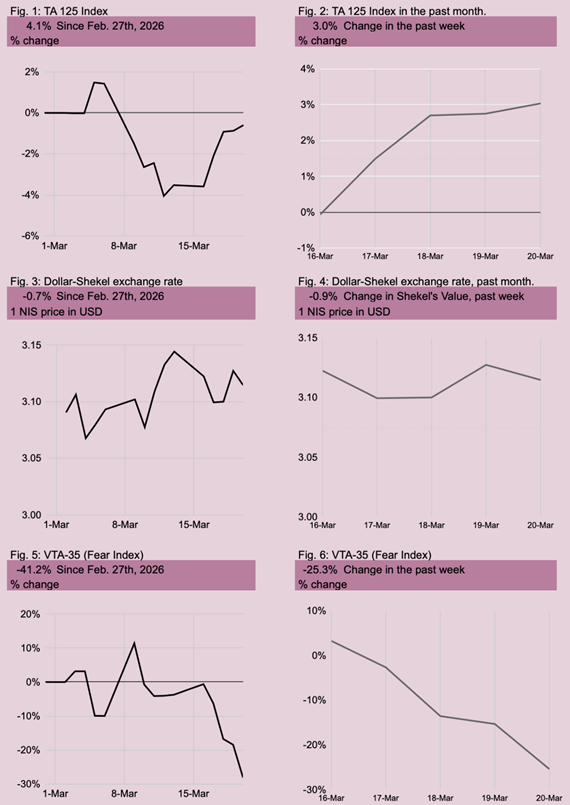

Alongside positive data for February, pointing to strengthening financial stability and a 3% gain in israel's TA-125 stock index, this week also saw the release of initial indicators relating to the wartime period.

February inflation data remained encouraging. Inflation over the past 12 months stood at 2%, exactly at the midpoint of the Bank of Israel’s target range. Inflation expectations for one year ahead also

remained low, ranging from 1.5% in the capital market to 2.2% in the forecasts of financial institutions.

The current account surplus rose sharply in the final quarter of 2025, and the Bank of Israel reported a 15.5% increase in the public’s financial assets, reaching approximately NIS 7.2 trillion.

Turning to wartime-related data, in an effort to maintain a lower deficit in light of the high costs of the fighting, the Ministry of Finance and The Association of Banks in Israel reached

an agreement on a one-time transfer of NIS 3.25 billion from the banks to the state, as an alternative to the tax changes discussed over the past year. This step is expected to bring the deficit

back to the original 2026 budget target of 4.9% of GDP, as set before the start of the operation.

A survey conducted by the Central Bureau of Statistics shows that, as in previous war situations, the biggest constraint on business activity is the closure of schools due

to the indiscriminate missile attacks on Israel. According to the survey, 42% of businesses reported that school closures are adversely affecting their operations. The survey also

indicates that the high-tech sector continues to demonstrate resilience and leadership. Since the start of Operation Roaring Lion, only 6% of businesses in high-tech and finance have reduced

employment due to the security situation, while 71% of these businesses continue to operate as usual. Around one-third of high-tech and finance companies expect no negative impact, and possibly even

an increase in revenues, in March. Across all sectors, only 4% of large businesses reported that the war had affected business activity or led to workforce reductions during the operation.

This week also marked meaningful progress in a strategic step to strengthen Israel’s high-tech sector. The Knesset Finance Committee approved the new R&D Law for second and third readings representing

a significant shift in the incentive structure for innovation. The law is designed to align the Israeli economy with the new global tax rules under OECD Pillar 2, while preserving substantial tax incentives

under the global minimum tax regime. If finally approved, the law will apply retroactively from the beginning of 2026 and will include enhanced benefits for companies that invest and establish activity

in Israel’s national priority areas.

Stay informed and stand with Israel,

Noach Hacker

|

Record-Breaking Investments

|

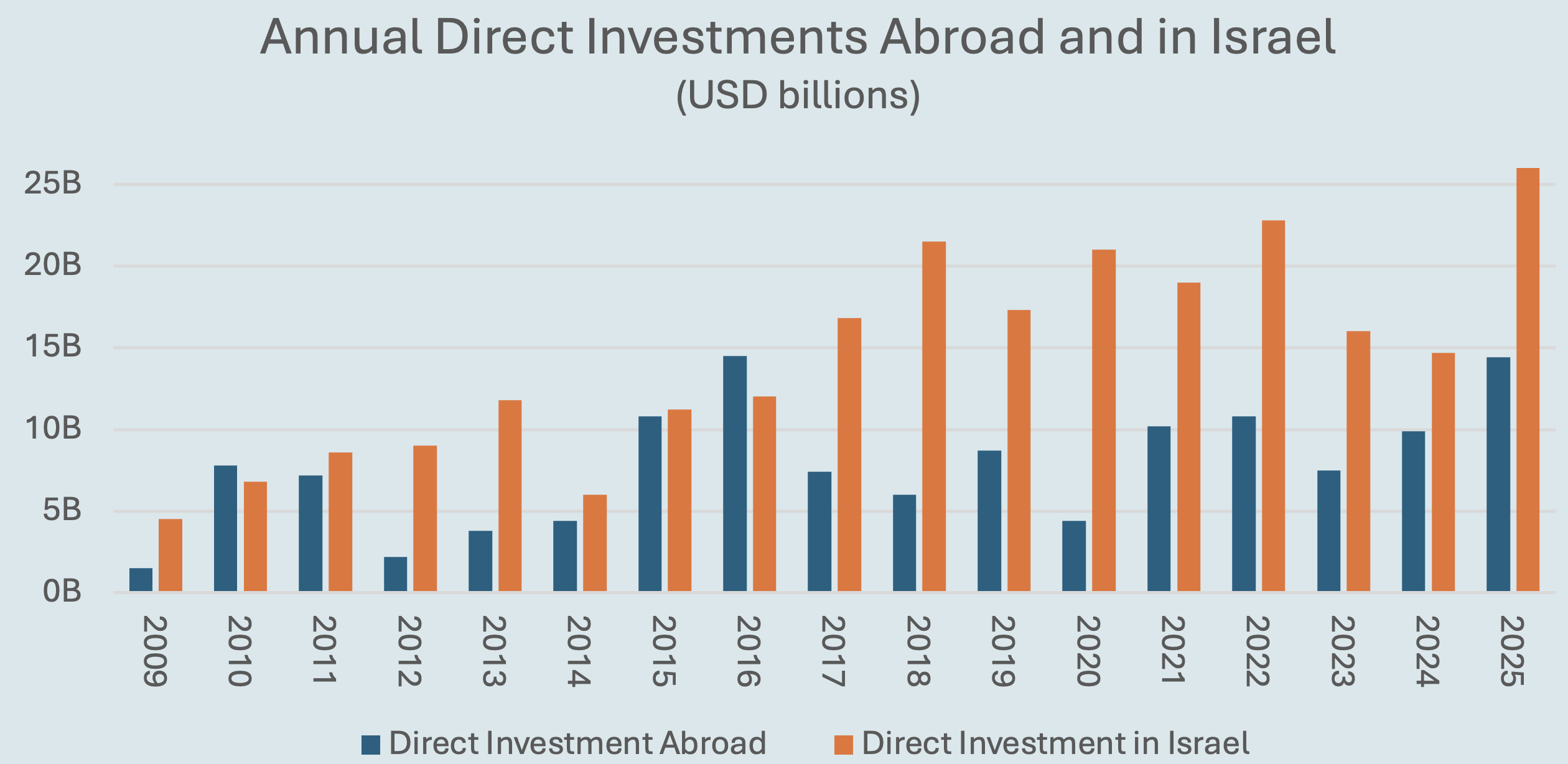

In 2025, direct investment abroad by Israelis rose by $14.5 billion, following increases of $9.9 billion in 2024 and $7.7 billion in 2023, while direct investment in Israel by foreign residents climbed to $26.2 billion, up from $14.8 billion in 2024 and $16.2 billion in 2023. This positive trend in two-way investment places 2025 among the strongest years on record.

|

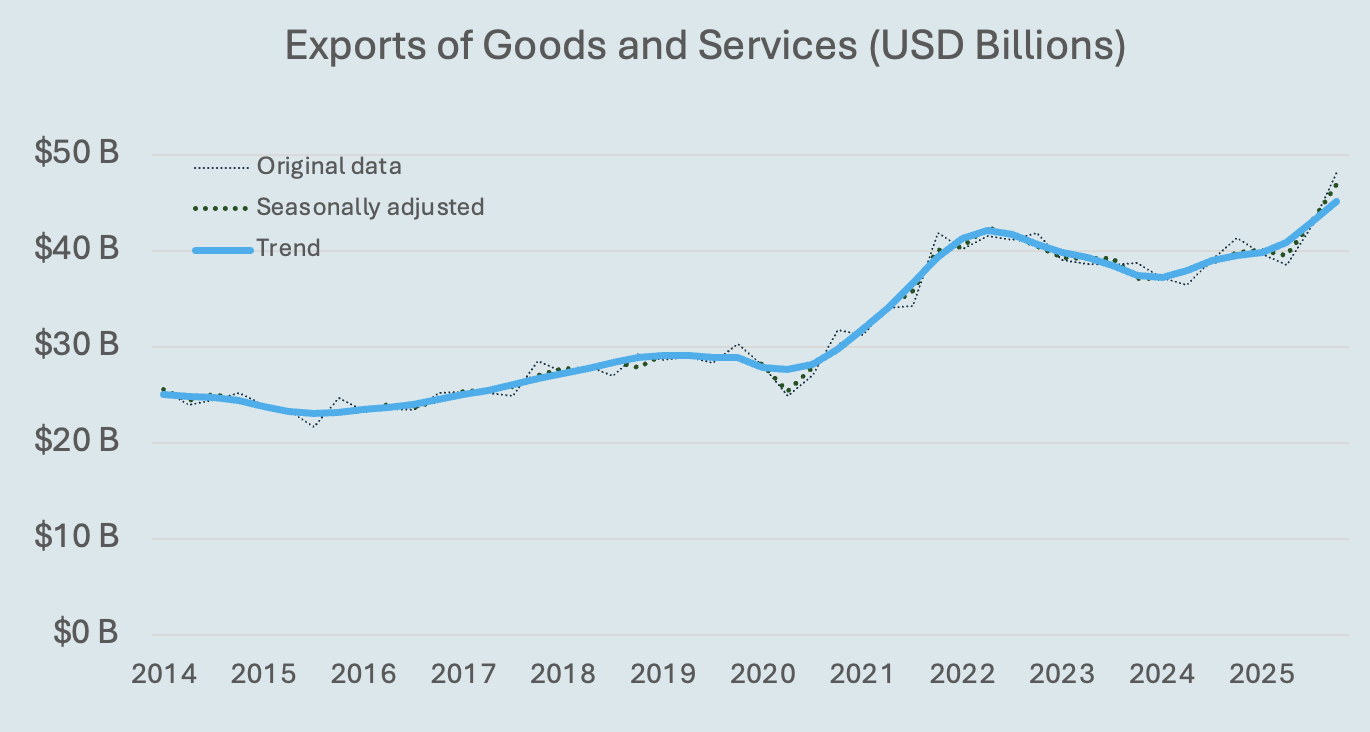

Israel’s exports of goods and services showed strong long-term growth over the past decade, rising from about $23.2 billion at the end of 2015 to $45.1 billion by the end of 2025, an increase of 94%. The trend also points to a rapid recovery after the Covid-affected year of 2020, followed by a strong expansion through 2022, and then another rebound from the dip in 2023 to record-high levels in 2025.

|

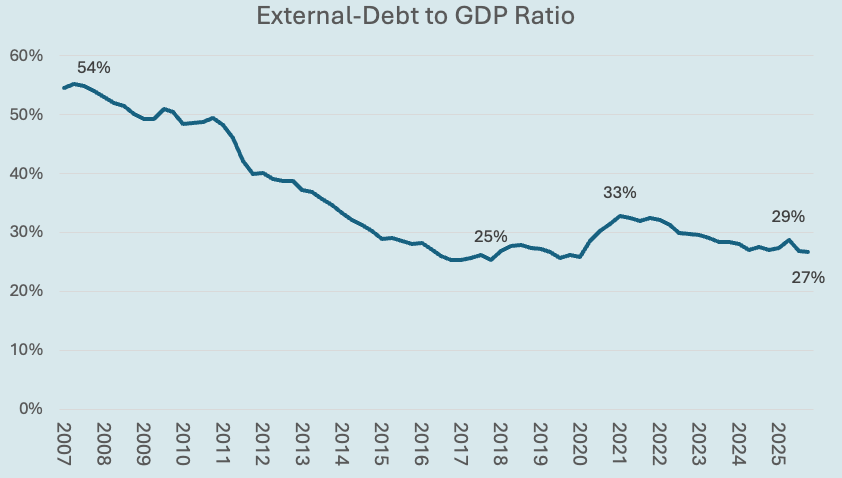

Israel’s external (foreign) debt as a share of GDP has declined sharply over the past two decades and stood at just 27% at the end of 2025, reflecting a major improvement in Israel’s external position. The only significant interruption came during the Covid pandemic, after which the ratio quickly shifted back to a downward path. While it edged up over the past two years because of the war, the increase had only a limited effect on the broader long-term trend.

|

|

|

|

|